Motorcoach Top 50 Tough Out Economy

FirstGroup America tops the list in METRO’s annual motorcoach survey, with 8,326 vehicles. The recession had business down overall, but operators forged ahead with more contract work and acquired new technological tools.

While last year's survey reflected a slight jump in business, averaging at 10 percent for two-thirds of coach carriers surveyed, 2009 played out differently for our Top 50 operators. Two-thirds of respondents reported that business was down compared to 2008, no surprise in the current economy. The average dip was 15.5 percent. Nineteen percent of carriers surveyed responded that their business had stayed even with 2008, and only four coach operators responded that business had increased in 2009 compared to 2008, with an average of six percent.

Efforts to increase business, as with last year, mostly involved pursuing contract work, with school contracts edging out government contracts this year - 40 percent and 34 percent, respectively. Fourteen percent diversified into limousine or paratransit.

Actions taken to offset costs were mainly fuel surcharges, at 54 percent, and rate increases at 44 percent. Staff downsizing rolled in at a distant third, at 30 percent. However, this was a significant spike when compared to 2008's 12 percent, showing the recession's impact on the industry.

Onboard amenities, such as satellite TV and Wi-Fi, were the most popular innovation this year with 29 percent of carriers saying they added these entertainment options to their coaches. Seven percent of operators reported adding GPS to their fleet, upgrading their Websites and joining Facebook and Twitter.

Once again, word of mouth proved to be the best reported marketing method, coming in at a whopping 50 percent, and soundly beating the Internet, which came in second, at 22 percent. Radio, TV and print ads and the Yellow Pages, the other options presented, barely registered, with each coming in at or below four percent. Other effective marketing outlets shared by surveyed operators were travel agents, tradeshows and operators using their own coaches as "rolling billboards."

Nearly one-quarter of operators cited pricing as their biggest challenge. "Our industry needs to be in a position to pay wages to attract high caliber staff," says Callen Hotard, president, of New Orleans-based Calco Travel/Hotard Coaches. The recession was certainly a contributing factor to the pricing hurdle, with 13.5 percent of operators choosing that option. Recruitment/retention and customer service both weighed in at 16 percent.

Ranking breakdown

A total of 15,283 vehicles, not counting vans (1,465) comprised this year's list. Motorcoaches totaled 49 percent, or 7,462, and non-motorcoach buses made up 51 percent, with 7,821 vehicles. The average fleet size is 139 vehicles, not counting the fleet of Dallas-based FirstGroup America, parent company of Greyhound Lines Inc., which surpassed all others in size, with a total of 8,326 coaches and non-motorcoach vehicles combined. The median fleet size is 82.

Twenty-seven operators plan to buy new vehicles in 2010, and 26 of those said they are looking to purchase vehicles with seat belts. Twenty-eight percent of respondents said they plan to acquire used vehicles in 2010. In all, operators reported plans to buy 188 new vehicles and 54 used vehicles, down significantly from last year.

FirstGroup America weighed in at the top of coach operators surveyed, moving up two spots from last year. (At press time, Coach America, a heavy-hitter typically in the top spot on our list, did not provide updated data). Coach USA occupied the second spot once again, with a total of 1,175 vehicles, slightly less than last year's report of a fleet of 1,800.

The list also changed slightly from last year, with some new additions, including New Orleans-based Calco Travel/Hotard Coaches, and Croswell VIP Motorcoach Services, located in Williamsburg, Ohio.

To view Top 50 list, click here.

More Motorcoach

Reinventing Fleet Maintenance with Real-time Visibility and AI

Transit leaders need to know what needs fixing, where to look, who is responsible, when work is completed, and what it costs without having to chase information across disconnected systems.

Read More →

ABA's Ferguson Testifies in Support of BUS Act, National Standards for Bus Operators

The BUSES Act would create a nationwide framework preventing state and local governments from enforcing bus idling restrictions of less than 15 minutes, a threshold consistent with existing Environmental Protection Agency guidance.

Read More →

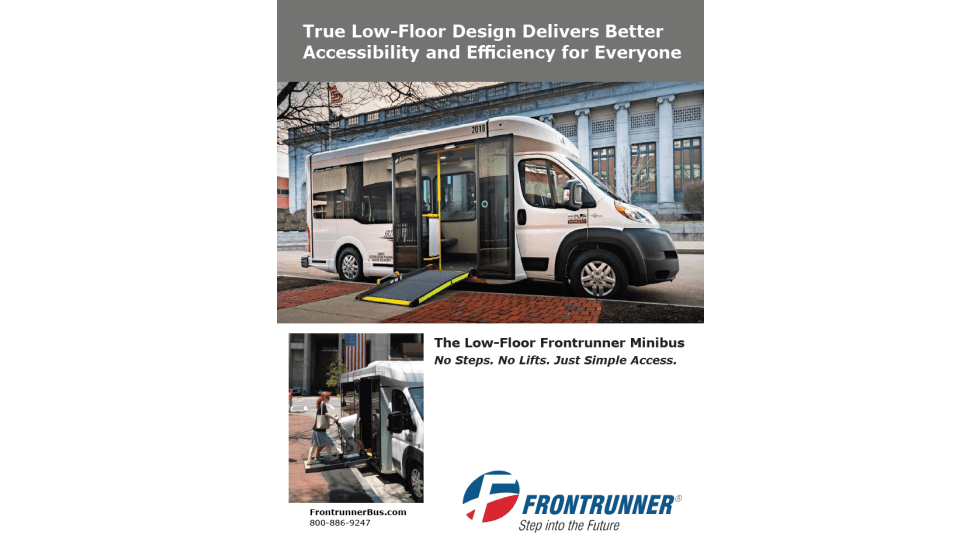

A True Low-Floor Minibus Design Delivers Better Accessibility and Efficiency for Everyone

As transit demands evolve, so should your fleet. Download the whitepaper to see how the Low-Floor Frontrunner Minibus compares to traditional options.

Read More →

2026 METRO Buyer’s Guide & Directory

Searching for the right vehicles, technology, equipment, or services for your public transit or motorcoach operation? This industry guide brings together manufacturers and suppliers from across the transportation market — all in one place. Download it to connect with the companies that help agencies and operators improve mobility, enhance operations, and move their organizations forward.

Read More →

ABA Foundation’s 2025 Motorcoach Census Highlights Industry Growth, 77K Jobs

Conducted annually by Tourism Economics, the study found that 1,769 companies operating 49,543 motorcoaches are based in the US, while 122 companies operating 1,425 motorcoaches are located in Canada.

Read More →

ENC Lands Additional 10-Bus Order From Academy Bus

The latest purchase brings Academy Bus’ AXESS fleet orders to 35 vehicles as ENC continues expanding its heavy-duty transit lineup.

Read More →

American Bus Association Files Lawsuit Against NYC Over Bus Idling Rules

The lawsuit, filed in the U.S. District Court for the Southern District of New York, challenges the City’s use of its Citizens Air Complaint program.

Read More →

Avoiding Mid-Season Breakdowns: A Fleet Readiness Q&A

John Hatman, COO of Master’s Transportation, breaks down the priorities, warning signs and common mistakes fleet managers should address now to stay ahead of summer demand.

Read More →

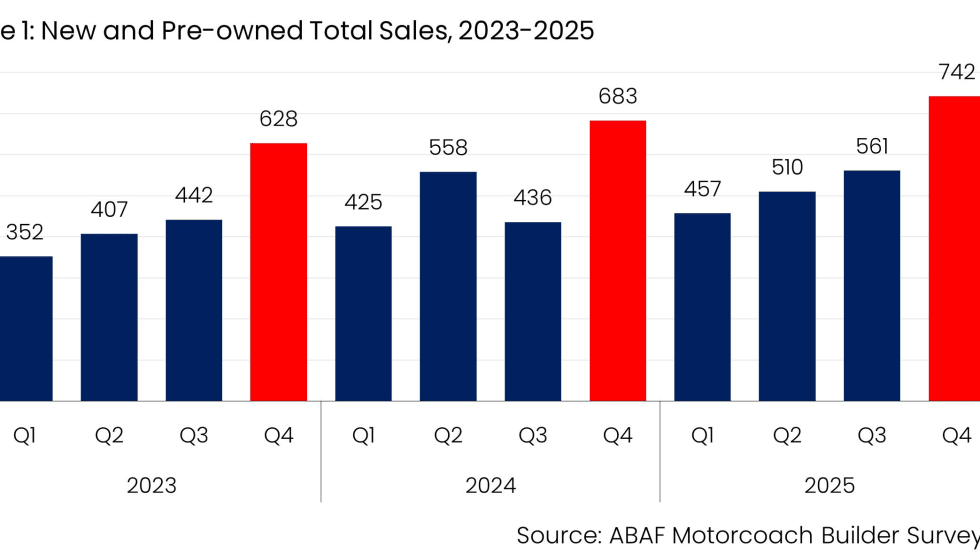

ABA Report: Motorcoach Sales Tick Up in Q1 2026 as Market Stabilizes

The Foundation produces the report each quarter, using data collected from surveys of major motorcoach manufacturers that sell vehicles in the US and Canada.

Read More →

How the Motorcoach Industry Supports Disaster Response and National Preparedness

Fred Ferguson, president and CEO of the American Bus Association (ABA), discussed how the industry prepares for emergencies, the growing recognition of motorcoaches as critical infrastructure, and steps operators can take to strengthen disaster readiness.

Read More →