How to Finance Your Motorcoach

Although business is still in the process of stabilizing and funds might still be tight, low interest rates and bonus depreciation make it a good time to purchase a new vehicle. According to lending experts, the single most important step to take is selling yourself on the idea first.

Before purchasing a new coach, it is a good idea to map out how it will be utilized, making sure that its use at least matches its financing term.

[IMAGE]MET11Financing-Coach-2.jpg[/IMAGE]Even with the somewhat stricter eye, many in the financing industry stress that, if an operator can qualify, now is a great time for financing a vehicle.

"Interest rates are at near historical lows and, the recently signed Small Business Act of 2010 brought back bonus depreciation and increased Section 179 expensing limits, so it's a great time to buy especially if you're in a taxpaying position," says Mike Denny VP/GM for MCI Financial Services Inc., which has also created two Webinars to help operators, available at its Website (www.mcicoach.com/service-support/webinars.htm), that focus on how to present your company to the financial community and bonus depreciation, respectively.

With the motorcoach industry beginning to slowly bounce back, it's possible, says Dave Johnson, regional sales manager at Key Equipment Finance, that a new replacement cycle is on the horizon for many operators, who he believes are taking a wait-and-see attitude to see if their bookings remain strong before investing in additional equipment. If that is the case, what can an operator do to make sure they get their coach purchase financed?

1. Sell yourself. Purchasing a new motorcoach is a big investment...are you sure you need it? Many of the lending experts we spoke with say the single most important step to take before seeking financing to purchase a new vehicle is selling yourself first.

"Just because you can get financing for a new motorcoach doesn't mean it's the best thing for our business," says Denny. "It's a long-term commitment, and we come across cases way too often where an operator bites off more than they can chew."

Before purchasing a new coach, it is a good idea to map out how it will be utilized, making sure that its use at least matches its financing term. In other words, if you are planning on using the new vehicle to simply fill a temporary void or service a short-term contract, think again.

"If an operator is picking up a unit because they are trying to accommodate a contract that lasts a month or two, it sounds foolish to a lender because, after that short-term contract is over, what are you going to do with the vehicle?" explains Eric Coolbaugh, vice president of Advantage Funding. "We just want to know that it's a sound, well thought out business move."

Ultimately, a motorcoach operations' ability to sell itself on the idea that purchasing a new vehicle is necessary will help in its goal to sell itself to the financial institution.

"You are asking the lender to make a sizeable investment in your company," says Peter King, vice president at TCF Equipment Finance. "You want to make sure the lender has a good feeling about the investment and your ability to pay back the loan."

Also, Johnson says it should be mentioned that you are not always just selling your operation financially.

"What I like to tell the operators is 'help me sell you.' We not only want to know how the vehicle will be used, but we like to know about the history of the company," he says. "Oftentimes, the operation was started by their grandparents and is now in its third generation, so it's nice to hear that story."

2. Understand what is needed. Be prepared to provide as much information as you can, including complete credit application, history of your business/business focus, business plan to include coach purchase justification, up to date business financial statements/tax returns, current fleet list and debt schedule, and personal financial statement and tax returns, Denny says.

King adds that interim financial statements with comparable statements from the same period for the previous year could be necessary as well.

In short, whether you are an old industry stalwart or just opening your doors be prepared to supply whatever is necessary, says Coolbaugh.

"We want to know where the company has been for the last three years and, if it hasn't been in business for three years, we want to know what they did previously," he explains. "If it's a start-up carrier, we want to know what type of delivery background they have and how they think they can support revenue for the asset they're looking to obtain. Also, if a company is in the business for a period of time, we want to know if this is an additional piece of equipment or if it is replacing an older piece they are getting rid of."

[PAGEBREAK]3. Finding a lender. Obviously, entering into a financing agreement is not a decision to be taken lightly and neither should your choice in a lender. Although many banks may offer loans, lenders stress that it's important to find somebody with a working knowledge of the motorcoach industry or, at the very least, the transportation business.

"Make sure your lender understands your business," says King. "The motorcoach industry is fortunate to have several active lenders that understand and support the industry."

Having a lender that understands the industry and what the significance is of purchasing a new lift-equipped vehicle, for instance, will help you not feel as if you are asking for "$500,000 and have three heads," states Coolbaugh. It also is a step toward what perhaps could be the most important tip, which is find a lender you can form a working relationship with.

"I often joke that lenders are like friends...you can never have too many. In the pre-9/11 era, most finance sources went deeper with each operator, meaning they were comfortable having more exposure," says Johnson. "A 20-coach operator may have had just one lender pre-9/11; now that 20-coach operator probably needs four or five financing sources, so it's important to have a good relationship with your lenders."

4. Have a plan. Have your books in order. Referring back to No. 1, most lenders simply want to know that an operator's wish to purchase a new vehicle is a well thought out decision.

"The first thing that we like and want to see is that the operator has a plan, so they are not just coming to us saying 'I need a bus,'" says Denny. "We want to know that they have thought it through, know where the revenues are going to come from and what the potential payments are going to be and, obviously, have already sold themselves."

Once you are sold on the purchase, it will help to understand what a lender looks for when extending credit, explains King. This list includes time in business, positive cash flow/debt service coverage, pay history, — both business and personal — reason for the equipment association (e.g. new contract or revenue sources), and if the finance term is in line with the expected useful life of the vehicle. King adds that other lender concerns may include leverage, or the amount of debt incurred vs. value of the company, and if the operation is growing too fast.

Once an operator knows what they are expected to bring and what a lender is looking for, it is important to submit an attractive, well put together package that they have taken the time to compile in a professional manner.

"If you come to me with a package that is well prepared and has great content, even if I see some blemishes in your package, I might be willing to overlook those because of the presentation," advises Coolbaugh.

One key step to creating an attractive package, which proverbially dots all the I's and crosses the T's, is having a professional on hand to handle your operation's books.

"A lot of operators are born into the business, it's in their blood and they do a great job of running their company but, sometimes it doesn't translate well when financials aren't presented in a professional manner," explains Johnson. "For an operator with five to 10 coaches or larger, it's a good investment to have professionally prepared financial statements, because it just helps better provide the entire picture."

MCI's Denny agrees with Johnson. "It's amazing how many times we get packages from customers that are looking for financing with information that is 18 months old. Without up-to-date financial information it becomes difficult to spot trends and make necessary changes that keep a business successful," he says. "This is the kind of a perspective that having a financial professional on hand can provide, so it's good for an operator to have somebody in that capacity that they trust."

5. Put away old misconceptions. Finally, it's important to keep in mind that things have changed, and what used to be a "slam dunk" isn't necessarily the case anymore.

"Many times, an operator thinks if they have made their payments on time it's almost like an auto approval," says Johnson. "While it's important to have a good pay history that in itself is not grounds for an approval."

King points out that another common misconception operators have is expecting that they do not need to make a down payment on their coach.

"Not only does this create more risk for the lender, but also makes the breakeven point several years out. This reduces the operators' options when it comes time to update equipment, since the operator may have little or no equity to put into the new deal," he says.

Other common misconceptions to consider before seeking financing include not needing to personally guarantee if your company is incorporated — personal guarantees are required with most motorcoach financing, says Johnson.

The biggest misconception to forget, though, is believing that credit is hard to obtain, according to lenders. As mentioned earlier, interest rates are currently low so, if your financials and business plan for the vehicle you are planning to purchase is sound, they say now could be the perfect time.

More Motorcoach

Reinventing Fleet Maintenance with Real-time Visibility and AI

Transit leaders need to know what needs fixing, where to look, who is responsible, when work is completed, and what it costs without having to chase information across disconnected systems.

Read More →

ABA's Ferguson Testifies in Support of BUS Act, National Standards for Bus Operators

The BUSES Act would create a nationwide framework preventing state and local governments from enforcing bus idling restrictions of less than 15 minutes, a threshold consistent with existing Environmental Protection Agency guidance.

Read More →

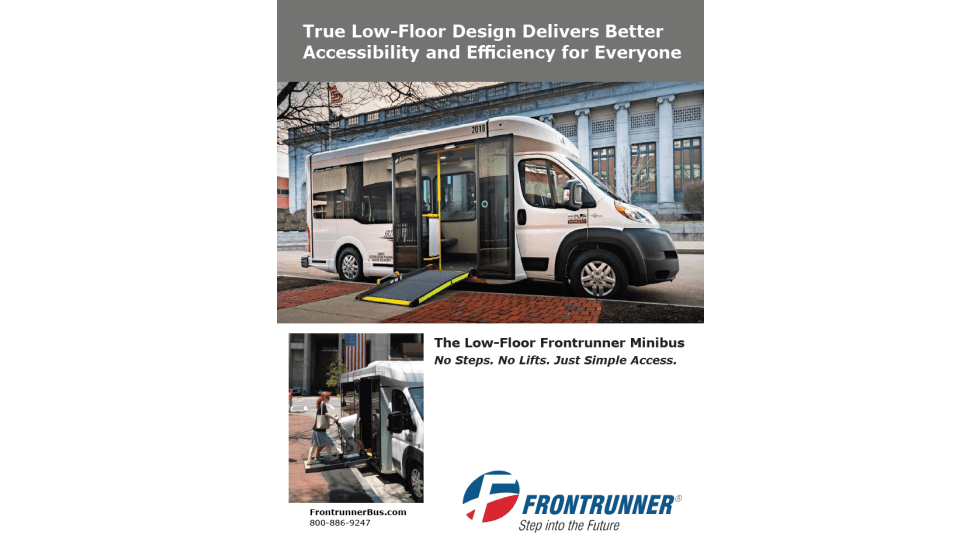

A True Low-Floor Minibus Design Delivers Better Accessibility and Efficiency for Everyone

As transit demands evolve, so should your fleet. Download the whitepaper to see how the Low-Floor Frontrunner Minibus compares to traditional options.

Read More →

2026 METRO Buyer’s Guide & Directory

Searching for the right vehicles, technology, equipment, or services for your public transit or motorcoach operation? This industry guide brings together manufacturers and suppliers from across the transportation market — all in one place. Download it to connect with the companies that help agencies and operators improve mobility, enhance operations, and move their organizations forward.

Read More →

ABA Foundation’s 2025 Motorcoach Census Highlights Industry Growth, 77K Jobs

Conducted annually by Tourism Economics, the study found that 1,769 companies operating 49,543 motorcoaches are based in the US, while 122 companies operating 1,425 motorcoaches are located in Canada.

Read More →

ENC Lands Additional 10-Bus Order From Academy Bus

The latest purchase brings Academy Bus’ AXESS fleet orders to 35 vehicles as ENC continues expanding its heavy-duty transit lineup.

Read More →

American Bus Association Files Lawsuit Against NYC Over Bus Idling Rules

The lawsuit, filed in the U.S. District Court for the Southern District of New York, challenges the City’s use of its Citizens Air Complaint program.

Read More →

Avoiding Mid-Season Breakdowns: A Fleet Readiness Q&A

John Hatman, COO of Master’s Transportation, breaks down the priorities, warning signs and common mistakes fleet managers should address now to stay ahead of summer demand.

Read More →

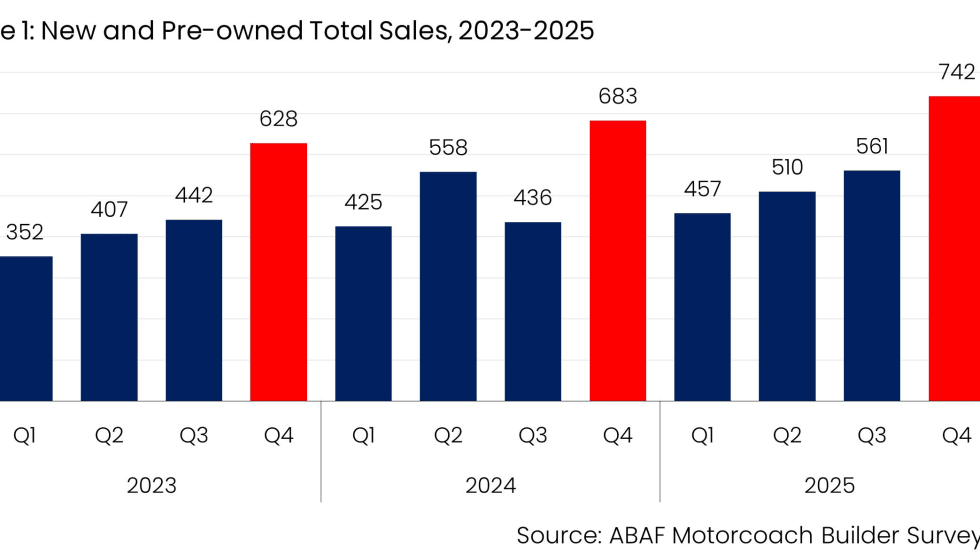

ABA Report: Motorcoach Sales Tick Up in Q1 2026 as Market Stabilizes

The Foundation produces the report each quarter, using data collected from surveys of major motorcoach manufacturers that sell vehicles in the US and Canada.

Read More →

How the Motorcoach Industry Supports Disaster Response and National Preparedness

Fred Ferguson, president and CEO of the American Bus Association (ABA), discussed how the industry prepares for emergencies, the growing recognition of motorcoaches as critical infrastructure, and steps operators can take to strengthen disaster readiness.

Read More →