With COVID Still In Play, Transit Bus Deliveries Down for 3rd Straight Year

While COVID and supply chain issues continue to make an impact on transit bus deliveries, the trend could shift in the short term thanks to record funding and the slow yet building increase in ridership around the nation.

The year-over-year propulsion mix can best be summarized by the surprising shift of alternate fuel deliveries being less than diesel, reversing the trend evidenced in 2021.

Photo: MBTA

For the third year in a row transit bus deliveries are down, however, with historic funding for zero emission buses and more, we expect to see an uptick over the next few years.

Chart: METRO Magazine

Calendar year 2022 again showed the sluggishness of the recovery in the heavy-duty transit bus segment in North America in terms of bus deliveries to the market. Although a continued slow recovery was forecasted for 2022 coming out of 2021, the data shows the market actually contracted for a third year in a row.

Further, gains made in alternate fueled vehicles — versus diesel propulsion — in prior years did not repeat themselves in 2022, as diesel propulsion vehicles regained the majority share in 2022. The 40-foot length bus segment continued to be the predominant vehicle delivered in 2022 rising in overall share versus 2021.

The sluggish deliveries in 2022 come as a surprise given the expectation was for a slow but steady increase in bus deliveries coming out of the COVID pandemic. Clearly, the challenges in returning the market to pre-pandemic delivery levels and the financial strain it causes for both operators and bus manufacturers are significant as both try to right the size of their operations for the current reality.

Overall Transit Bus Market Assessment

There were several surprising findings in this year's delivery numbers, including:

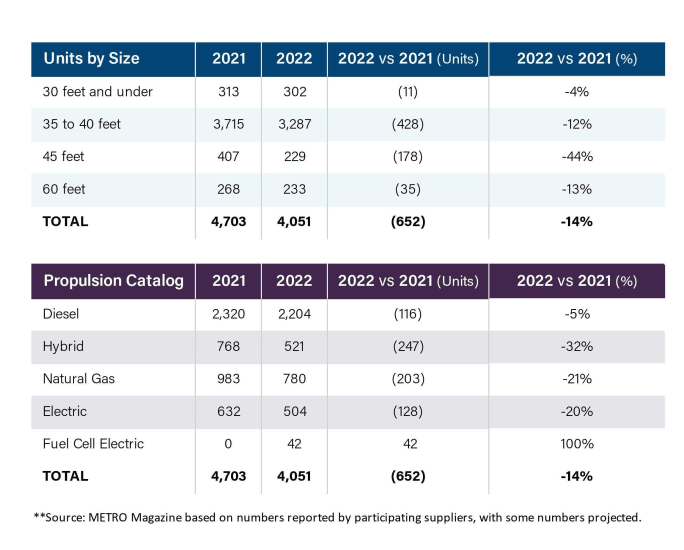

2022 vs 2021 overall transit bus production declined by 652 units, or 14%, from 4,703 units in 2021 to 4,051 units in 2022. As a reference, market deliveries pre-pandemic in 2019 were 6,320 units, and thus, the market is delivering only 64% of pre-pandemic units. Interestingly, there is a parallel with the level of ridership at transit agencies in 2022, which averaged between 60% to 70% compared to pre-pandemic levels.

Primary possible reasons for the decline in 2022 are: continued challenges and tailwinds with supply chain materials, chip shortages for electrical components, shipping logistics, and maintaining staffing levels at bus production facilities.

Further complications arose from fleets not needing buses that were under contract due to reduced ridership, as well as contractual negotiations where OEMs looked to renegotiate pricing given the significant cost increases that have been incurred from the COVID pandemic. These issues quite probably delayed deliveries in many cases.

It is still understood new bus bid volume continues to be healthy, especially for electric vehicles.

Although 2022 was expected to be improved from 2021 for bus deliveries, we will see what 2023 brings as the march out of the pandemic continues to be a tough, challenging, and lumpy climb back to industry health for operators and bus manufacturers.

Assessment from a Transit Vehicle Length Segmentation Perspective

Overall, 40-foot transit bus deliveries made up the majority of the vehicles delivered. Trends by vehicle size included:

30-foot and under units experienced a minor decline of 11 units, or 4%, in 2022 from 313 units in 2021 to 302 units in 2022.

35- to 40-foot units experienced a significant reduction of 428 units, or 12%, from 3,715 units in 2021 to 3,287 units in 2022. Given that 40-foot buses are the predominant length of a bus in the market, it stands to reason this segment experienced the largest volume decline in 2022.

45-foot units experienced the worst percentage decrease of 44%, or 178 units, from 407 units in 2021 to 229 units in 2022.

60-foot units experienced a moderate decline of 35 units, or 13%, from 268 units in 2021 to 233 units in 2022.

The year-over-year changes show that the 35- to 40-foot segment continues to be the primary vehicle length for the market, with 81% of the volume in 2022 versus 79% in 2021. The 45-foot segment took the largest hit in 2022, reducing to 6% compared to 9% of the overall market in 2022.

Assessment from a Transit Bus Propulsion Segmentation Perspective

Surprisingly, the trend toward alternative-powered vehicles delivered outlegging diesel changed in 2022. Some of the findings from this year's survey, include:

All propulsion-type volumes were negatively affected in 2022 compared to 2021, however, some much more than others. 2021 was the first year where alternate fuel-powered vehicle deliveries exceeded diesel deliveries. In 2022, that trend ended with diesel deliveries exceeding alternate fuel deliveries by 357 units.

Electric propulsion vehicle deliveries waned by 20% in 2022, from 632 units in 2021 to 504 units in 2022.

Diesel propulsion continues to maintain the majority of market demand, as noted above, with only a minor decrease of 5% compared to 2021, from 2,320 units in 2021 to 2,204 units in 2022.

Trolley and fuel-cell electric propulsion showed no units in 2021 which was consistent with 2020.

Trolley deliveries were again zero units in 2022 same as in 2021.

2022 is the first year in the recent past where hydrogen fuel-cell electric deliveries were achieved with 42 units being delivered.

Hybrid propulsion saw the largest year-over-year decline of 32%, from 768 units in 2021 to 501 units in 2022.

The year-over-year propulsion mix can best be summarized by the surprising shift of alternate fuel deliveries being less than diesel, reversing the trend evidenced in 2021. This may well be because these alternate fuel vehicles utilize very specific and low-volume components, which may have been more adversely affected by supply chain issues than diesel buses.

In conclusion, 2022 proved to be yet another challenging year for the transit bus market segment with a decline in the volume of vehicles delivered for the third straight year.

Diesel propulsion was the main power source in 2022, reversing a trend seen in 2022 where alternate-fueled vehicles were the majority share of the market.

For 2023, we will see how things land with the slow and clunky recovery from the pandemic in 2020, but expect the amount of alternatively-propelled vehicles to begin to grow again as usage across the nation continues to take hold and Low-No and other vehicles funded by the Feds begin to be delivered.

METRO would like to thank all our suppliers for taking part again in this year’s survey.

More Bus

Biz Briefs: STV teams with Amtrak, Motorcoach Operators Boost Fleet and Land Contracts, and More

From manufacturers and suppliers to transit agencies and motorcoach operators, these updates offer a snapshot of the projects, partnerships and business moves driving the industry forward.

Read More →

LA Metro Marks Banner Year, Sets Ambitious Goals for New Fiscal Year

Incoming LA Metro Board Chair and Los Angeles Mayor Karen Bass joined outgoing Board Chair Fernando Dutra and LA Metro CEO Stephanie Wiggins to review accomplishments from fiscal year 2026, which included the opening of new rail extensions, advancement of major transit projects, expanded safety programs, and new rider amenities.

Read More →

DART Taps Nathaniel P. Ford Sr. as Next President/CEO

Since 2012, Ford has served as the CEO of the Jacksonville Transportation Authority

Read More →

AC Transit’s Cecil Blandon on Building the Next Generation of Transit Maintenance Leaders

The agency’s maintenance chief discusses leadership, workforce development, zero-emission technology, and preparing technicians for the future of public transportation.

Read More →

Building the Next Generation of Transit Technology

In this edition of METROspectives, Luminator CEO Magnus Friberg discusses the company's transformation, the growing role of AI and software, and what's next for transit technology.

Read More →

June LA Metro Ridership Surges 2 Million Year Over Year

Total June ridership increased for both weekdays and weekends. Weekday ridership was 953,820, which grew 8.4% from June 2025; Saturdays increased nearly 13% year-over-year to 708,826; and Sundays increased 7.7% to 611,534 from June 2025, according to LA Metro.

Read More →

Washington's Pierce Transit Board Sends Transit Funding Measure to November Ballot

With the adoption of Resolution 2026-006, the measure moves to the Pierce County Auditor, giving voters in the Pierce Transit service area the decision on whether to fund an expansion of local transit service within the agency’s service area.

Read More →

New York Unveils Sweeping Plan to Modernize City Bus Service

Next Stop: Fast Buses, Better Service identifies 50 priority bus corridors for improvements across the five boroughs and launches the City’s next generation of rapid bus service along five key routes.

Read More →

CTDOT Taps STV for Electric Bus Facility Design

The firm will work with CTDOT and RVT to define the facility layout, operational requirements, and long-term flexibility for RVT’s growing electric fleet.

Read More →

Ford to Leave JTA After More Than 10 Years as CEO

He plans to continue his work advancing innovative mobility solutions to improve the quality of life in communities across the nation. He did not announce specific plans.

Read More →