2013 Motorcoach Top 50 Expand Fleets, Training

Business was up in 2012 for the majority of respondents. While FirstGroup America and Coach USA still hold the top two spots, Horizon jumps up to number three.

For METRO’s 2012 Top 50 Motorcoach operators survey, we expanded our reach and received input from a total of 106 carriers. Therefore, our list is shaken up, somewhat. American Coach Lines of Orlando, AFC Transportation and Colonial Trailways are a few of the handful of companies that are new to the list this year.

This time around, we also added ques-tions about marketing segments, seat belts and refurbishment, to get a better-rounded snapshot of the industry.

Rankings

Fleet sizes among the top respondents were larger in general this year. FirstGroup America-Greyhound Lines Inc. and Coach USA, as usual, took the first and second spots, respectively. Dallas-based Horizon Coach Lines moved up to the third spot, from the eighth position it held last year, after purchasing about 900 coaches from the now bankrupt Coach America in September.

New Britain, Conn.’s DATTCO moved up four spaces, to grab the number 10 spot, and Silverado Stages, based in San Luis Obispo, Calif., broke into the top 20, jumping from number 21 last year to 18 this year.

A total of 22,276 vehicles are represented among the Top 50 operators in this survey. Among all respondents, the vehicle total is 23,621.

The average fleet size among the 50 largest operators, not counting FirstGroup and Coach USA, is 143. The median fleet size is 82.

Forty-three of the Top 50 operators, or 86%, have plans to buy more vehicles this year, the same as last year. Slightly more than three-quarters of operators made estimates on their buying plans for 2013, with the remaining quarter having firm plans in place. The most popular vehicle brands selected were Motor Coach Industries (29%), Prevost (20%) and Van Hool (16%).

Business increasing

Business in 2012 was up for more than three-quarters of the Top 50 motorcoach operators and for 64% of all respondents. On average, for the Top 50, the increase was 12%. Business was down for only 3% of operators, and for nearly 20%, it stayed the same.

To increase business, two-thirds of carriers obtained government contracts, 57% took on private company contracts, and about one-half partnered with other coach operators and secured school contracts. Twelve percent diversified into limousine or paratransit service.

Actions taken to offset costs included rate increases by nearly three quarters of operators, fuel surcharges (66%), staff downsizing (15%), reductions in services (8%), and reduced idling and advance fuel purchases (4% each).

Once again, the most favored marketing method was word of mouth at 64%. The Internet trailed this year among our Top 50, selected by only 20%, down by more than 10% from last year. Social media, in particular, was favored by nearly 10%. Additional methods cited were client referrals, direct sales (2% each) and trade shows (1%). While about 3% of all respondents said they used radio, print and TV ads, none of our Top 50 used those marketing methods, and no operators reported using the Yellow Pages.

One new survey question addressed marketing segments operators made a special effort to reach. Eighty percent chose universities; about one-half selected seniors, sports teams, and church and religious groups; and about one-third selected commuters. [PAGEBREAK]

Innovations

Wi-Fi and GPS were the most popular innovations cited, with one-third installing them this year, a slightly higher number than in 2011.

Approximately one-fifth added electronic onboard recorders or iPads for driver convenience in compliance tracking, and 8% added 100-volt outlets and created apps. Lakeland Bus Lines of Dover, N.J. enhanced the user-friendliness of its website, particularly with capability to send status alerts to customers’ phones. Another operator that has been on the Top 50 list in the past, Sebring Fla.’s Annett Bus Lines, installed technology on its coaches to let customers track their buses in real time.

Challenges

The biggest challenge carriers said they faced in 2012 was hiring, training and retaining good drivers who understand customer service. Perhaps in response, more than 80% of the Top 50 operators, and about three-quarters of all operators surveyed, stepped up driver training in customer service, (27%), ADA requirements (31%), and to a lesser extent, eco-driving (6%).

About one-quarter of operators struggled with pricing and operation costs, and slightly more than 10% faced the obstacles of competing with low-ball operators and keeping up with regulations.

We asked again this year about whether coach carriers think that the federal government’s focus on motorcoach safety is effective. Three-quarters responded yes, which was the same response as last year. Those who were not convinced that the safety efforts would pay off once again said that enforcement is the real issue, with rogue operators not being targeted enough and upstanding operators being unfairly penalized.

Additionally, providers noted that more focus needs to be placed on the driver and not the vehicle and equipment such as seat belts. As one operator put it, “I’ve been on plenty of buses with seat belts. No one wears them, so how can it improve safety?”

Seat belts

This year, we asked about the portion of vehicles with factory-installed seat belts in operators’ current fleets. Only 6% of the Top 50 operators said their entire fleet, or nearly their entire fleet, had the belts installed. Thirty-two percent responded that 1% to 10% of their vehicles were equipped with seat belts, one-fifth said that 11% to 20% of their vehicles had seat belts, and about one-fifth have no factory-installed seat belts in their fleets.

Eighty percent of carriers said they plan to add motorcoaches with factory-installed seat belts to their fleets in 2013. About two-thirds of operators claimed to only be interested in buying buses with factory-installed belts.

Refurbishment

We also included new questions about refurbished coaches. Three-quarters of operators responded that they have refurbished coaches in their fleets. The average number of refurbished vehicles among those surveyed and in the Top 50 is seven. Operators that are considering buying refurbished coaches in the next year totaled to about three-quarters. Carriers who said they are not looking into buying refurbished coaches in 2013 responded that they refurbish in-house (33%), only buy new, mostly due to contract requirements (33%), don’t have money in the budget this year to buy any vehicles (22%) or think it’s too expensive (3%).

For the full story as it appeared in print, click here.

More Motorcoach

Reinventing Fleet Maintenance with Real-time Visibility and AI

Transit leaders need to know what needs fixing, where to look, who is responsible, when work is completed, and what it costs without having to chase information across disconnected systems.

Read More →

ABA's Ferguson Testifies in Support of BUS Act, National Standards for Bus Operators

The BUSES Act would create a nationwide framework preventing state and local governments from enforcing bus idling restrictions of less than 15 minutes, a threshold consistent with existing Environmental Protection Agency guidance.

Read More →

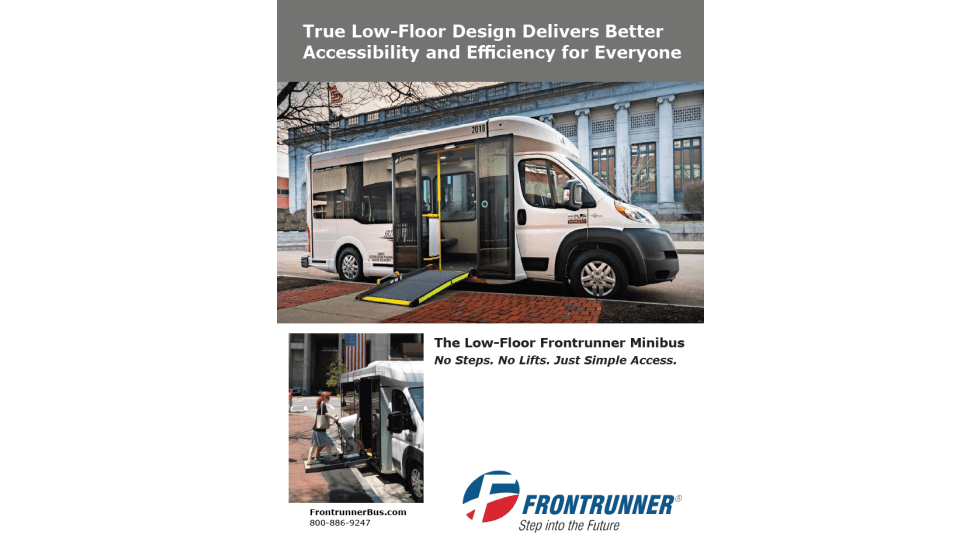

A True Low-Floor Minibus Design Delivers Better Accessibility and Efficiency for Everyone

As transit demands evolve, so should your fleet. Download the whitepaper to see how the Low-Floor Frontrunner Minibus compares to traditional options.

Read More →

2026 METRO Buyer’s Guide & Directory

Searching for the right vehicles, technology, equipment, or services for your public transit or motorcoach operation? This industry guide brings together manufacturers and suppliers from across the transportation market — all in one place. Download it to connect with the companies that help agencies and operators improve mobility, enhance operations, and move their organizations forward.

Read More →

ABA Foundation’s 2025 Motorcoach Census Highlights Industry Growth, 77K Jobs

Conducted annually by Tourism Economics, the study found that 1,769 companies operating 49,543 motorcoaches are based in the US, while 122 companies operating 1,425 motorcoaches are located in Canada.

Read More →

ENC Lands Additional 10-Bus Order From Academy Bus

The latest purchase brings Academy Bus’ AXESS fleet orders to 35 vehicles as ENC continues expanding its heavy-duty transit lineup.

Read More →

American Bus Association Files Lawsuit Against NYC Over Bus Idling Rules

The lawsuit, filed in the U.S. District Court for the Southern District of New York, challenges the City’s use of its Citizens Air Complaint program.

Read More →

Avoiding Mid-Season Breakdowns: A Fleet Readiness Q&A

John Hatman, COO of Master’s Transportation, breaks down the priorities, warning signs and common mistakes fleet managers should address now to stay ahead of summer demand.

Read More →

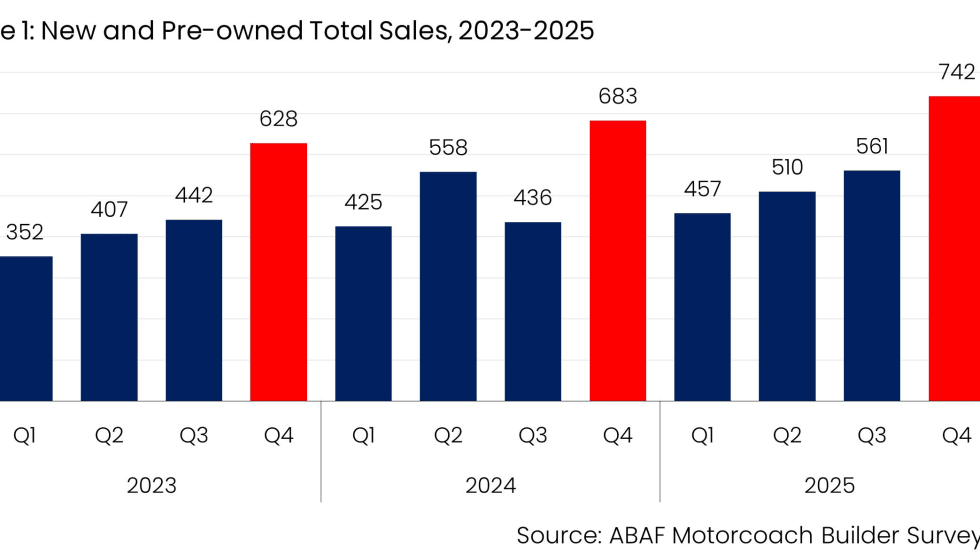

ABA Report: Motorcoach Sales Tick Up in Q1 2026 as Market Stabilizes

The Foundation produces the report each quarter, using data collected from surveys of major motorcoach manufacturers that sell vehicles in the US and Canada.

Read More →

How the Motorcoach Industry Supports Disaster Response and National Preparedness

Fred Ferguson, president and CEO of the American Bus Association (ABA), discussed how the industry prepares for emergencies, the growing recognition of motorcoaches as critical infrastructure, and steps operators can take to strengthen disaster readiness.

Read More →